Your team is busy. Calendars are packed, Slack never stops, and project leads keep saying they need more capacity. Then finance closes the month and the margin isn't there.

That gap usually isn't a mystery. It's a measurement problem.

In agencies, people often assume that if staff are fully booked, revenue should follow. It doesn't. Work only turns into profit when you capture it, bill it correctly, and collect it on time. If any part of that chain breaks, the agency leaks revenue while everyone still feels overloaded. That's why realization rate calculation matters so much. It ties daily delivery work to cash in the bank.

What is a realization rate and why it matters more than you think

Monday looks full. The delivery team is booked, account managers are juggling client requests, and every calendar says the agency is at capacity. Then the month closes and profit comes in light.

That usually points to realization.

A realization rate measures how much of your agency's potential billable revenue turns into cash. In plain terms, it answers a harder question than utilization does: out of all the work your team could have billed at standard rates, how much of that money did the agency collect?

That makes realization an operating metric with financial consequences. A low rate rarely starts in finance. It usually starts upstream, in how work gets scoped, how time gets captured, how invoices get adjusted, and how fast clients pay. If leaders only look at booked hours, they miss the leak.

I've seen this in agencies with strong demand and tired teams. The staff are busy, clients are active, and project leads keep asking for more headcount. But a chunk of the value never survives the trip from calendar to timesheet, from timesheet to invoice, or from invoice to cash receipt.

Typical causes are familiar:

- Scope drift: extra requests get handled without a revised estimate or change order.

- Late or weak time capture: people fill in hours from memory and miss short but billable work.

- Pre-invoice write-downs: managers cut time to avoid client pushback.

- Collection friction: invoices go out late, approvals stall, or clients pay well past terms.

That is why realization matters more than many agency operators expect. It ties day-to-day execution to margin. It also shows whether the team has a sales problem, a delivery problem, or a process problem.

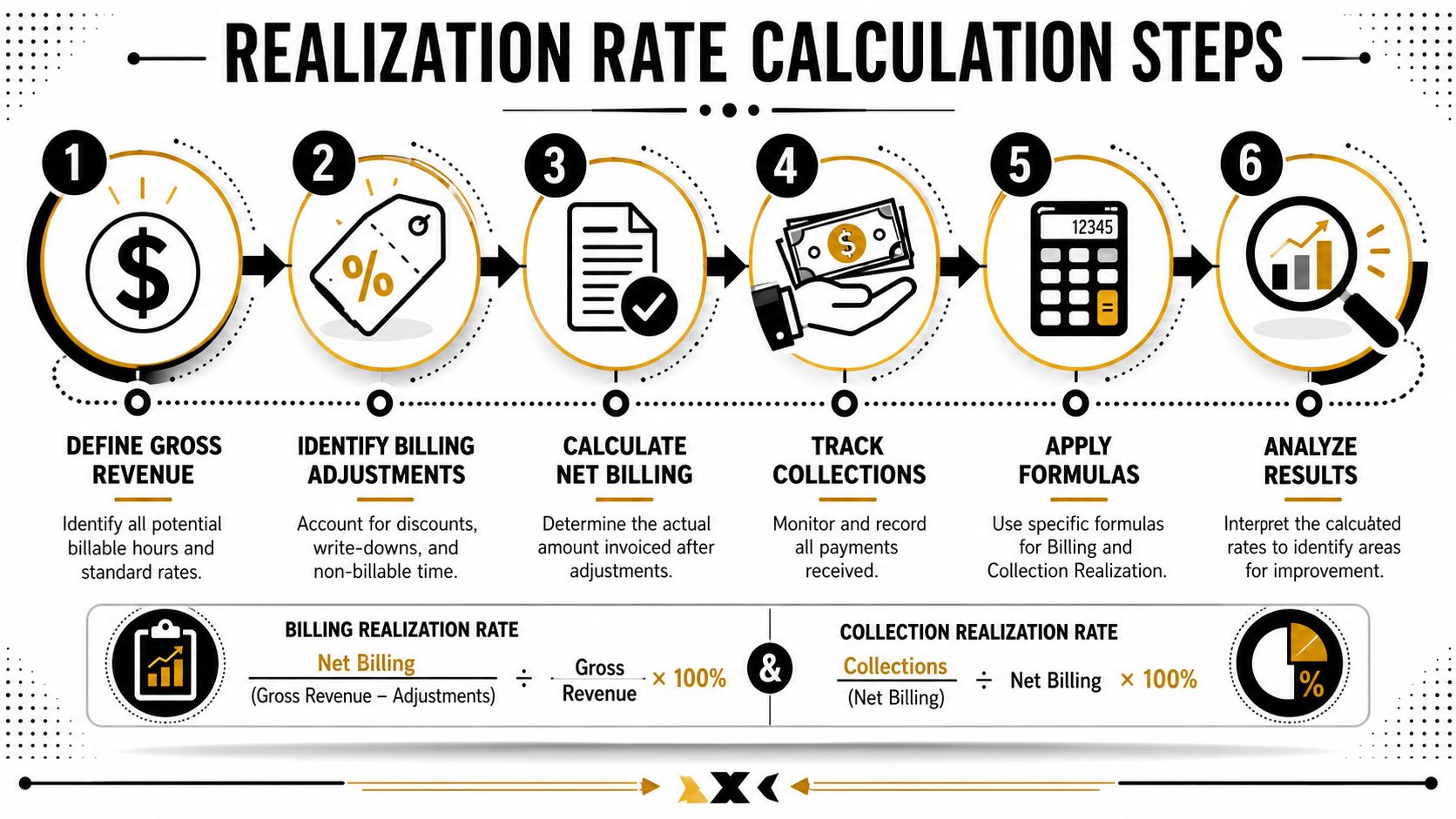

At the highest level, the calculation is simple:

Actual revenue collected / potential billable revenue

The hard part is getting reliable inputs. Agencies that rely on manual timesheets and end-of-week reconstruction often calculate realization too late and with bad source data. Calendar-based activity tracking gives operations and finance a cleaner starting point because it captures the meetings, work blocks, and client touchpoints that staff forget to log later. That does not replace review and coding discipline, but it cuts the manual overhead that distorts the number in the first place.

If you're trying to boost your marketing returns, realization deserves a place next to client ROI and account profitability. Revenue growth looks healthy on paper until write-downs, missed hours, and delayed cash collection strip out the margin.

The same logic applies to your time data. A stronger process for tracking billable hours gives you the raw material for an accurate realization rate, and lets you spot revenue leakage while there is still time to fix it.

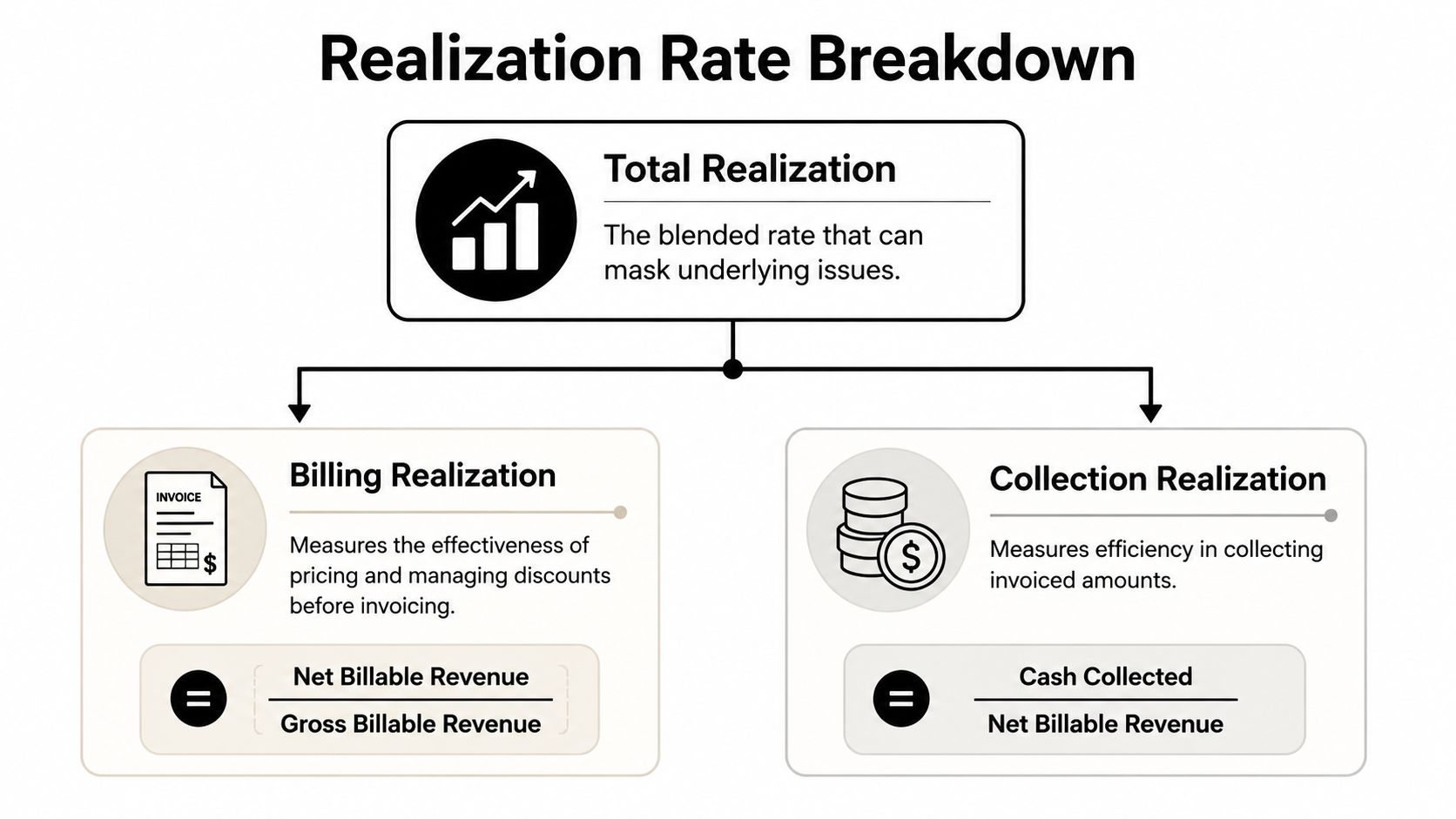

The exact formulas for billing and collection realization

A single realization number is not enough to run an agency well. Finance needs to know where revenue is leaking before margin disappears at month-end.

Split the metric into two parts. Billing realization shows how much of the value your team created made it onto an invoice. Collection realization shows how much of that invoice turned into cash.

The two formulas that matter

Here's the visual breakdown.

Use these formulas:

- Billing realization: net billable revenue / gross billable revenue

- Collection realization: cash collected / net billable revenue

- Overall realization: cash collected / gross billable revenue

Agencies that still review time in hours can calculate the same thing from hour-based inputs:

- Billing realization: invoiced billable hours / worked billable hours

- Collection realization: collected amount / invoiced amount

The math is simple. The hard part is getting clean inputs.

Gross billable revenue starts with the work your team performed at standard rates. Net billable revenue reflects what survived write-downs, fee caps, unapproved overages, and unbilled time. Cash collected is the amount the client paid. If any one of those numbers is weak or delayed, realization drops.

Why splitting the rate changes how you manage

Billing realization usually breaks first inside delivery. Time is logged late. Project leads trim hours to avoid a difficult client conversation. Work happens in Slack, meetings, and review rounds, but never gets coded properly. By the time finance sees the file, the agency has already given away revenue.

Collection realization usually breaks in billing operations and accounts receivable. Invoices go out after the work is no longer fresh in the client's mind. Backup is incomplete. Purchase order details are missing. A client disputes the bill, and cash gets pushed into the next month or quarter.

Those are different problems with different owners.

That distinction matters in real operations. If billing realization is weak, fix scoping, time capture, approval discipline, and write-down behavior. If collection realization is weak, fix invoice timing, documentation, follow-up cadence, and payment terms.

Manual tracking distorts the formula

This metric gets unreliable fast when the agency relies on reconstructed timesheets and spreadsheet rollups. People forget what happened on Tuesday. They round hours on Friday. Account managers clean up entries before invoicing, and finance ends up calculating realization from edited history instead of raw activity.

Calendar-based tracking gives operations a better starting point because it captures the meetings, work sessions, and client touchpoints that usually disappear in manual logging. It does not replace review. It does give billing and finance a real-time record of what happened, which makes gross billable revenue more accurate before write-downs start.

That is also why realization should be read alongside how to calculate utilization rate. Utilization tells you whether paid staff time is being spent on client work. Realization tells you whether that work survives your delivery and billing process long enough to become revenue.

A healthy agency watches both. High utilization with weak realization means the team is busy but the operation is leaking money between the calendar, the invoice, and the bank account.

A step-by-step worked example of a calculation

Monday starts with a client workshop. By Friday, the team has also handled two extra revision calls, a few Slack requests, and a last-minute deck cleanup before the presentation. None of that looks expensive while the work is happening. It becomes expensive when some of it never makes it into the bill, or gets written down before the invoice goes out.

That is why a worked example matters. The math is simple. The hard part is tracing what happened across calendars, time entries, invoice drafts, and cash receipts.

Start with the raw work value

Use one client account for one month.

Say the agency delivered work across strategy, design, and account management. Pull the record of billable activity first, then value that work at standard rates before anyone trims the invoice.

Here are the inputs:

- Worked billable hours: Time spent on client work

- Standard billing rates: Normal rates by role

- Gross billable revenue: Worked billable hours multiplied by standard rates

- Billing adjustments: Write-downs, courtesy discounts, capped fees, or unbilled time

- Net billable revenue: What the agency invoiced

- Cash collected: What clients paid

That sequence matters because each handoff creates a chance to lose revenue.

Walk through the calculation

Assume the team's month of client work adds up to $40,000 at standard rates. That is gross billable revenue.

Before invoicing, the account lead removes $4,000 in extra revision time and applies a $2,000 discount to keep renewal discussions easy. The invoice goes out for $34,000. That is net billable revenue.

By month-end, the client has paid $28,000. The rest is still outstanding because one invoice is late and one line item is under dispute.

Now calculate each rate:

Billing realization = net billable revenue / gross billable revenue

Billing realization = $34,000 / $40,000 = 85%

Collection realization = cash collected / net billable revenue

Collection realization = $28,000 / $34,000 = 82.4%

Overall realization = cash collected / gross billable revenue

Overall realization = $28,000 / $40,000 = 70%

That 70% number is the one leadership feels in the P&L.

The team produced $40,000 worth of billable work. The business only collected $28,000 during the period. The missing $12,000 did not disappear in one place. It leaked out across write-downs, discounting, invoicing, and collections.

What this example shows in practice

An ops lead looking at those numbers should ask two separate questions.

First, why did $6,000 disappear before invoicing? That points to scope control, service discipline, weak change-order habits, or hours that were never captured cleanly enough to defend.

Second, why did another $6,000 fail to convert to cash during the period? That points to invoice timing, client documentation, dispute handling, or payment follow-up.

This split is what makes realization rate useful operationally. It does not just show that revenue is low. It shows where the process is leaking.

The input quality problem

A lot of agencies try to run this calculation from reconstructed timesheets and spreadsheet summaries. That creates a measurement problem before finance even touches the formula.

If strategists log time from memory on Friday, the gross billable number starts soft. If project managers trim entries before anyone reviews the original activity, operations loses the audit trail. If finance receives a cleaned-up invoice draft instead of the raw work record, realization gets calculated from edited history.

Calendar-based tracking fixes part of that problem by giving operations a time-stamped record of meetings, work blocks, and client touchpoints as they happen. It gives finance and delivery a more accurate starting point for gross billable revenue, especially on accounts where the leakage comes from small tasks nobody bothers to enter manually.

What to pull from your systems each month

For a calculation you can trust, gather:

- From tracking data: billable hours by person, client, and project

- From calendars or activity records: meetings, calls, and work sessions that confirm what happened

- From project operations: approved overages, capped fees, discounts, and write-downs

- From billing: invoice amounts by client and billing period

- From finance: cash receipts applied to those invoices

Once those five pieces line up, the calculation stops being an abstract finance metric. It becomes an operating report. You can see whether the loss happened because the team did unbilled work, because managers cut the bill, or because collections lagged after the invoice went out.

Common pitfalls and adjustments that destroy your rate

Agencies don't usually lose revenue in one dramatic event. They lose it in small operational choices that feel harmless at the time.

A senior strategist jumps on an extra call. A designer makes one more round of edits. An account manager says, “Don't worry, we'll take care of it.” None of that looks serious in isolation. On the invoice, it becomes serious.

Scope creep is the obvious leak, but not the only one

Everyone talks about scope creep because it's easy to spot after the fact. The bigger issue is poor capture.

If work changes and nobody updates the scope, the team still does the work. That means labor cost goes up while billable value stays flat. The realization rate drops, and leadership often blames pricing when the actual problem is process.

The same thing happens with tiny tasks. Five-minute Slack requests. Two “quick” review calls. A deck clean-up before a client presentation. Teams often skip these because logging them feels annoying. Over time, those skipped fragments become a real amount of lost revenue.

Pre-bill write-downs create a false sense of client happiness

A lot of agencies use invoice trimming as a relationship tool. Someone reviews the draft bill and says it feels too high, so they cut hours before the client ever sees them.

That move can be sensible in a few cases. Most of the time, it hides a delivery problem:

- the scope was weak

- the team over-serviced the account

- the work took longer than planned

- nobody warned the client early

Pre-bill cuts protect the conversation this month, but they train the client to expect extra work without cost. Then the same account gets less profitable every quarter.

Operator's note: If you keep fixing bad scopes with write-downs, the agency will look busy and underperform at the same time.

Aging WIP is where collectability starts to rot

One of the fastest ways to hurt realization is to let completed work sit unbilled.

CoralTree points out that aging work-in-progress is a primary cause of low realization. When billing cycles lag 30+ days behind work cycles, or when unbilled work sits beyond two to three weeks after completion, the ability to collect full value degrades in its WIP and realization discussion.

That lines up with what most operators see in practice. The longer you wait:

- project context fades

- clients forget the urgency

- PMs cut more time to avoid pushback

- finance spends more effort explaining old work

Here's a simple view of how common mistakes map to the metric:

| Pitfall | Billing realization | Collection realization |

|---|---|---|

| Scope changes without approval | Hurt | Can also hurt |

| Late time entry | Hurt | Indirectly hurts |

| Invoice sent long after work finished | Hurt | Hurt |

| Vague invoice narrative | Sometimes hurts | Hurt |

| Client discount to “save the account” | Hurt | Usually neutral |

What actually works

Strong agencies don't rely on heroics here. They use operating habits that reduce ambiguity.

- Lock billing cadence: Invoice on a fixed rhythm and protect it.

- Review WIP early: Don't let old unbilled work pile up.

- Push change orders fast: If the work changed, the paper has to change too.

- Train PMs on margin: Client service without financial discipline isn't service. It's leakage.

Realization falls when the agency avoids hard conversations. It improves when the agency handles those conversations while the work is still fresh.

Benchmarking your rate and setting realistic goals

A COO reviews month-end and sees a realization rate that looks acceptable on paper. Then the detail comes out. One account team is writing off hours every cycle because scope approvals happen late. Another is billing too slowly because time is still trapped in calendars, chat threads, and half-finished timesheets. The blended number hides both problems.

That is why benchmarking matters. A target gives the team a reference point, but its primary value is diagnostic. It helps you tell the difference between a pricing problem, a delivery problem, and a tracking problem.

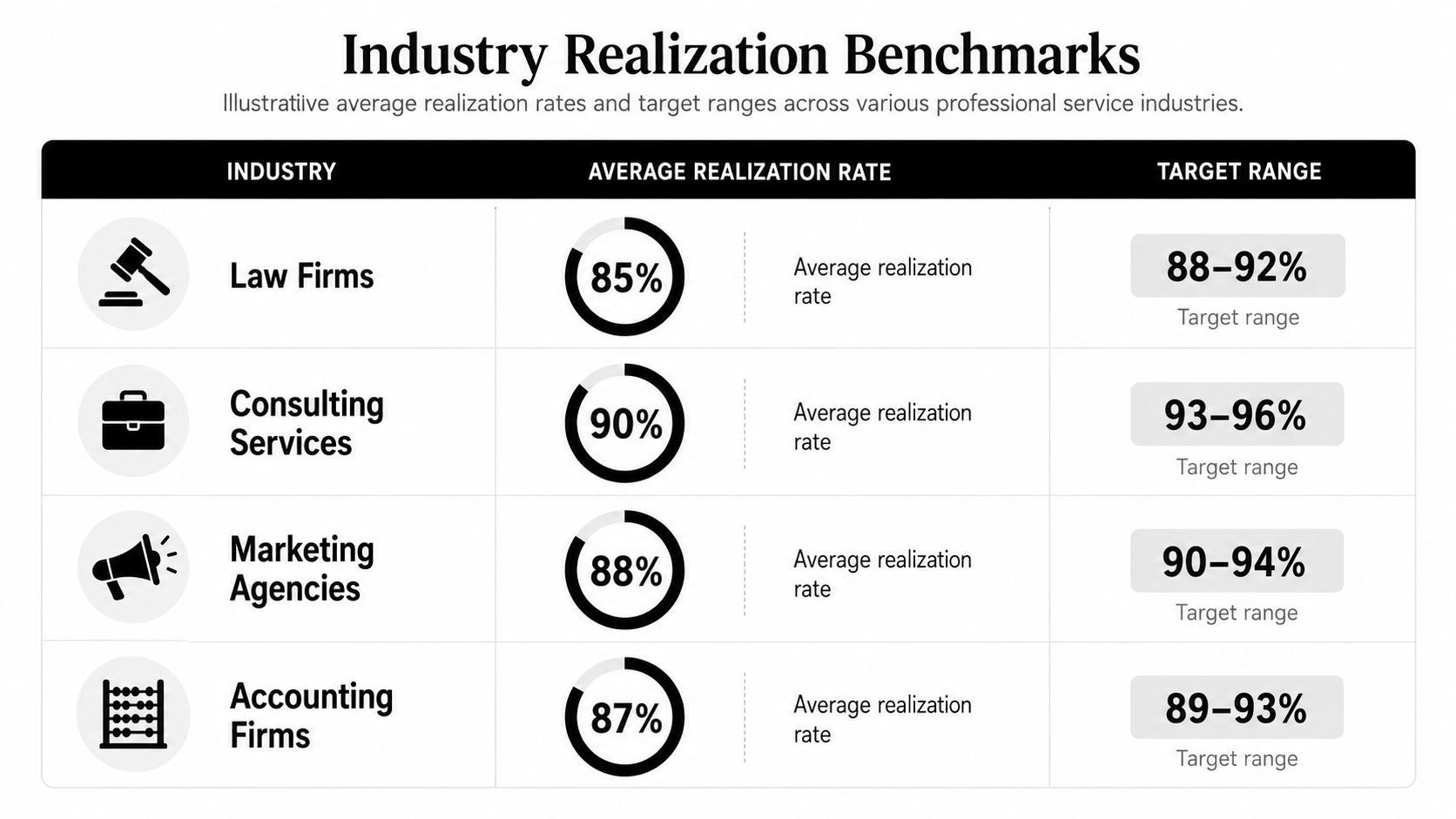

What outside benchmarks can and cannot tell you

Here's the benchmark visual.

Adjacent professional services categories give useful context, even if agencies should not copy them blindly. Earlier in the article, the law firm benchmark showed a clear split between average performers and firms with tighter billing discipline. Architecture firms also report very high realization when time capture and project tracking are handled well, according to Monograph's architecture realization benchmark.

The lesson is practical. A few points of realization are not rounding error. They usually point to recurring operating behavior.

If your rate is lower than you expected, ask what your team is doing every week that creates write-downs, delays invoices, or weakens collections. That question gets you to the fix faster than comparing yourself to a prettier industry average.

Set targets by operating reality, not wishful thinking

A healthy goal depends on how your agency runs:

- pricing model and contract type

- retainer work versus project work

- frequency of scope changes

- billing cadence

- approval speed between delivery, account management, and finance

- quality of time capture before invoices are drafted

An agency with fixed monthly retainers and tight scope control can hold a higher target than an agency doing custom project work with constant revision cycles. An agency with manual timesheets and Friday memory-based entry should not expect elite realization right away. The first priority is getting a number you can trust.

A realization target only helps if the input data reflects the work that actually happened.

That is where operations teams get tripped up. Leaders set a 95% target, but the team still tracks time manually, updates WIP late, and rebuilds the week from memory. The target is fine. The operating system underneath it is not.

A practical way to set goals

Use a staged approach tied to the cause of leakage.

- Stage 1: Establish a believable baseline. If calendars, meetings, and work sessions are not captured cleanly, start there. Agencies using automated timesheet software usually get a more reliable baseline because the record starts with actual calendar activity instead of end-of-week recall.

- Stage 2: Separate billing realization from collection realization. If billing is weak, focus on scope control, approvals, and invoice timing. If collections are weak, fix invoice clarity, client communication, and follow-up.

- Stage 3: Raise the target in steps. Improve by a few points, hold the gain, then push again. That is more durable than declaring a top-tier target while the same old write-off habits stay in place.

For most agencies, the right benchmark process starts with a blunt question. Is the rate low because the team is underbilling good work, discounting avoidably, or failing to capture the work in the first place? Once you know that, goal-setting stops being abstract and starts driving margin.

From manual tracking to automated insight

Manual timesheets create bad inputs.

That's the operational truth underneath most realization problems. People forget what they did, especially when their day is split across client calls, internal reviews, Slack messages, and quick edits. By Friday, they reconstruct the week from memory. Then finance tries to build clean revenue reporting from that pile of estimates.

The math can be perfect and still be useless if the underlying data is guessed.

Why manual entry breaks down

Most professional services organizations use 2,080 hours as the traditional standard for total available hours, based on 40 hours/week × 52 weeks/year, while a common alternative is 2,000 hours based on 50 weeks/year, according to Beyond Software's utilization explanation. That denominator matters for utilization first, and utilization feeds the broader revenue picture.

But the denominator isn't the hardest part. Capturing the numerator is.

A typical agency employee's day includes:

- scheduled client meetings

- internal project check-ins

- focused work blocks

- short admin tasks

- reactive requests that interrupt planned work

Manual timesheets miss the edges of that day. People round down. They forget small tasks. They delay entry until details blur. The result is underreported work, weak billing support, and endless cleanup by ops.

What better raw data looks like

A stronger system captures work closer to when it happens and reduces the need for memory-based entry. Calendar-based tracking is useful because the calendar already holds a large part of the truth for service teams. Meetings, booked work blocks, recurring client touchpoints, and project patterns are already there.

That doesn't remove human review. It improves the starting point.

Here's what that kind of workflow looks like in practice.

![]()

When agencies move away from pure manual entry, three things usually get better:

- Coverage improves: More of the workday gets captured, especially fragmented work.

- Speed improves: Teams spend less time filling timesheets and ops spends less time correcting them.

- Confidence improves: Leaders trust the realization rate because the raw data is less dependent on memory.

Why this changes the management conversation

Once time capture gets cleaner, realization stops being a backward-looking accounting exercise. It becomes an operating signal.

You can see where work is happening, what was likely billable, what still sits in WIP, and which client teams are drifting into under-recovery. That's a much better conversation than telling people to “do their timesheets better.”

If your agency is stuck in spreadsheet cleanup and late reporting, start with systems that reduce entry friction and improve visibility. Tools built for automated timesheet software can give ops teams a more reliable base for utilization, billing review, and realization reporting without adding more admin to the delivery team.

If your agency wants cleaner time data without the usual timesheet fatigue, TimeTackle is worth a look. It uses the calendar as the starting point for time capture, which helps teams log work with less friction and gives operations leaders better data for utilization, billing, and realization analysis. That means fewer end-of-month guesses, less manual reporting overhead, and a more reliable view of where revenue slips before it reaches the invoice.