Month-end in a mid-sized agency often looks the same.

Finance has one spreadsheet. Delivery has another. Account managers swear a milestone is done, but the project lead says the client asked for one more round. Someone exported time entries on Tuesday, someone else changed the scope on Wednesday, and by Friday the revenue number is still moving.

That mess is not just annoying. It changes how you see the business. If recognized revenue is off, margin looks wrong, utilization decisions get distorted, and leadership starts making calls from half-clean data.

Most rev rec software content talks to SaaS companies with neat subscription schedules. Agencies do not work like that. Your revenue often depends on hours worked, milestones accepted, retainers consumed, and change requests approved. That means the accounting answer depends on operational proof, not just billing logic.

The familiar chaos of agency revenue reporting

A common agency scene goes like this. The CFO asks for a clean month-end number. The PMO starts chasing status updates. Finance exports billing data, then tries to match it to contracts that were edited in email, approved in Slack, and partially tracked in a project tool.

The deeper problem is not the spreadsheet. The problem is that agencies often split the truth across systems. Sales owns the signed deal. Delivery owns the work. Finance owns the ledger. Nobody owns the bridge between them.

Where agencies get stuck

Runeleven points out that existing content on this topic is mostly built around SaaS subscriptions and usage billing, while missing the system design problems agencies deal with, especially reconciling time entries with revenue schedules and handling scope changes tied to tracked work (Runeleven on revenue recognition software for agencies).

That gap matters because agency contracts are rarely clean and static. A retainer can include strategy, production, revisions, and overages. A fixed-fee implementation can drift into support work before anyone rewrites the statement of work. By the time finance sees the contract reality, the month is already closing.

What manual reporting hides

Manual rev rec tends to hide four things:

- Delivery slippage: Revenue may look earned on paper even when the team is still finishing work.

- Profitability by client: If hours and milestones do not reconcile, margin by account gets fuzzy.

- Forecast quality: Next month’s expected revenue turns into a rough guess instead of an operating number.

- Audit defensibility: When someone asks, “Why did you recognize this amount in this period?” the answer lives in email threads.

A good rev rec setup for an agency is not just an accounting tool. It is a way to prove what was delivered, when it was delivered, and how that maps to the contract.

When agency owners say they want better forecasting, fewer timesheet battles, and cleaner month-end closes, they are usually asking for the same thing. They need a system that ties operational data to financial recognition without forcing finance to rebuild the story by hand every month.

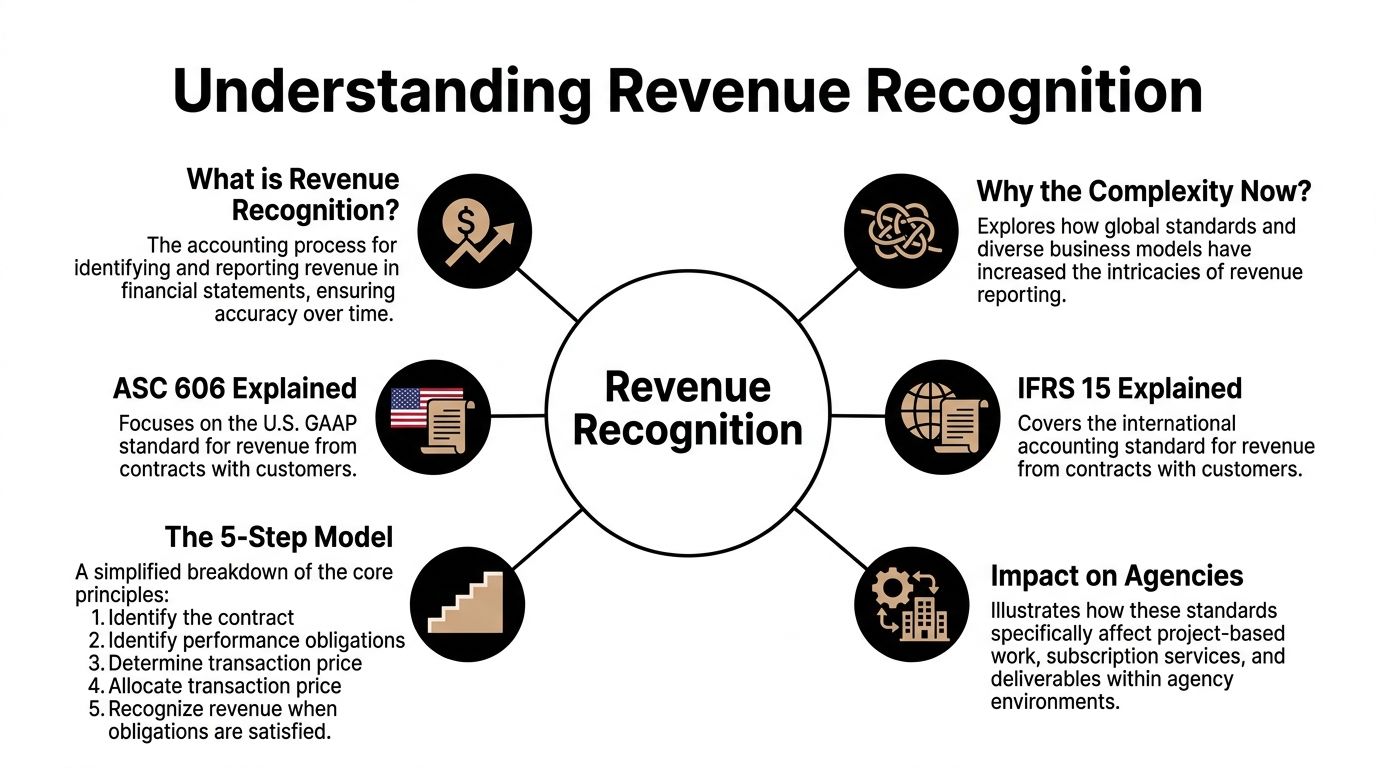

What is revenue recognition and why is it so complicated now

Revenue recognition is the rule for when you can count revenue. Not when cash arrives. Not when an invoice goes out. When you have earned it.

That sounds simple until you look at how agencies sell work.

If a client prepays a quarterly retainer, you cannot always treat the full invoice as earned on day one. If a project includes discovery, implementation, training, and ongoing support, you may not recognize all of it on the same timeline. The accounting follows delivery.

The plain-English version of ASC 606 and IFRS 15

ASC 606 is the main U.S. standard for revenue from customer contracts. IFRS 15 is the international version. Both push companies toward the same idea. Recognize revenue when you satisfy what you promised the customer.

For an agency, that promise might be:

- a strategy workshop

- a website launch

- a monthly retainer covering a service period

- a block of implementation work

- support or customization that runs over time

The standard uses the term performance obligation. In normal language, that means a promised piece of work the client is paying for.

The five-step model without the jargon

Many teams do not need a textbook explanation. They need a way to think clearly. The five-step model is:

- Identify the contract. What did the client agree to?

- Identify the promised deliverables. What distinct work are you on the hook to provide?

- Determine the transaction price. What is the value of the deal after discounts, changes, and variable elements?

- Allocate that price. How much of the total belongs to each deliverable?

- Recognize revenue as each promise is met. Not before.

A contractor analogy helps. If you are hired to remodel a kitchen, install lighting, and build custom cabinets, those may not all be earned at the same moment. Payment terms matter for cash. Delivery terms matter for revenue.

Why this gets hard for agencies fast

The hard part is not the five steps. The hard part is mixed contracts.

Moss Adams notes that under ASC 606, unbundling multi-element arrangements like software access plus implementation services can shift reported revenue timing and amounts by up to 20-30% in complex contracts, and misclassifying 15-25% of professional services can lead to audit adjustments averaging $500K-$2M for mid-sized firms (Moss Adams revenue recognition guide for technology companies).

Agencies face the same kind of judgment calls even when they are not selling software. A project might include setup work, production work, and advisory work. Some items are distinct. Some are tightly linked. If you classify them badly, the timing changes.

The old shortcuts break down

A lot of agencies still operate with informal rules such as:

- “Recognize the retainer monthly.”

- “Recognize project revenue when invoiced.”

- “If the client paid, book it.”

Those shortcuts feel fine until contracts become layered. Then finance has to decide whether implementation is separate from the main service, whether a milestone is complete, or whether overages count now or later.

Revenue recognition got harder because service businesses sell more hybrid contracts than they did before. The accounting now asks for a level of precision that spreadsheets rarely hold for long.

Once you see revenue recognition as a delivery problem with accounting consequences, rev rec software starts to make more sense. It is not there to make finance look advanced. It is there to turn messy contract reality into consistent rules.

Core features every agency needs in rev rec software

Most agency teams do not need every enterprise finance feature on the market. They need a system that can survive real project work, contract drift, and messy delivery evidence.

Start with one contract record

If the contract terms live in sales notes, a PDF, and a billing platform, the software will never be better than the inputs.

A solid platform needs one place to store:

- contract dates

- pricing terms

- milestone structure

- scope changes

- credit notes or amendments

For agencies, this is what stops the monthly “which version is final?” argument.

Rules engine first, dashboard second

Good demos often lead with polished dashboards. That is fine, but the rules engine matters more.

You want software that can handle:

- fixed-fee milestones

- time and materials

- monthly retainers with caps or overages

- hybrid contracts that mix project work and support

If the tool only works cleanly for straight-line schedules, it will force your team back into spreadsheet workarounds. Errors creep in there.

Reporting that operations can use

Finance reports alone are not enough. The best setups let operations and delivery leaders see what has been earned, what is deferred, and what is at risk.

That matters because the business question is rarely “Are we compliant?” The question is, “Did we earn what we thought we earned, and can we trust the next forecast?”

If you are also reviewing the broader systems around forecasting and handoff quality, this guide to best RevOps software is useful because it frames how revenue data moves across sales, ops, and finance instead of treating each function as a silo.

Audit trail is not optional

Agencies often underweight this until the first painful audit cycle.

The software should keep a clear record of:

- who changed contract terms

- when a milestone was marked complete

- what source data triggered recognition

- how a schedule changed after a scope amendment

That record is what turns a judgment call into a defensible process.

If a vendor cannot show you how the system handles a contract change mid-month, keep looking. Agency revenue rarely stays still long enough for static schedules.

A final test is whether the platform can work with your billing workflow, not fight it. Agencies that bill from service data often need a path from activity capture to invoicing to recognition. Purpose-built tools around billing software for professional services can help you think through the operational side, not just the accounting output.

Connecting your tech stack for accurate revenue data

Rev rec software does not fix bad inputs. It just processes them faster.

That is why agencies struggle when they buy a revenue tool before they clean up the data path. If the CRM says one thing, the PSA says another, and the accounting platform gets a third version, recognition logic starts from a bad premise.

The stack that matters

For most professional services firms, the revenue data chain has four parts.

| System | What it contributes | Why finance cares |

|---|---|---|

| CRM | Contract terms, pricing, start dates | This is the commercial intent |

| Project or delivery system | Milestones, task status, scope changes | This shows whether promised work moved |

| Time tracking layer | Hours, activity categories, effort by client | This is often the proof of performance |

| ERP or accounting system | Journal entries, deferred revenue, reporting | Recognition lands here |

A weak link in any one of those systems creates cleanup work downstream.

Why time data matters more than many finance teams expect

For agencies, time data is often the cleanest evidence that work happened. Not perfect evidence. But better than a vague status field.

If a contract is time and materials, hours are the revenue driver. If it is milestone-based, activity logs often support whether a milestone is complete. If it is a retainer, time and activity data tell you whether delivery matched what the contract assumed.

Agencies usually feel the operational gain first here. Revenue follows approved work instead of a delayed admin process.

That is why integration with project and activity tools matters. Many teams start by connecting the delivery side more tightly through project management integrations, then use that data to clean up the downstream accounting logic.

Variable work creates variable accounting

Chargebee notes that for usage-based contracts, ASC 606 requires revenue to be constrained to probable amounts, which can distort MRR metrics by 10-35% if unmodeled. The same source says automating feeds from time records and project milestones can achieve 95% forecast accuracy, and that rev rec leads with ERP integration experience reduce implementation cycles by 30-50% while automating up to 80% of allocation rules (Chargebee guide to SaaS revenue recognition).

Even if your agency does not think of itself as “usage-based,” many contracts behave that way. Overage hours, variable support, change requests, and milestone acceptance delays all create moving recognition inputs.

What works and what does not

What works is a single flow of contract, work, and ledger data with clear ownership. Sales owns the commercial terms. Delivery owns completion evidence. Finance owns policy and review. The systems carry the record between them.

What does not work is asking finance to infer delivery from invoices alone. In agencies, invoices often reflect what was billed. Revenue recognition asks what was earned.

The cleanest revenue number usually comes from the least dramatic process. Good integrations remove debate because the system already knows what changed, when it changed, and which rule should apply.

Sample workflows for professional services firms

The easiest way to judge rev rec software is to walk through the contracts you already sell. If the workflow breaks on normal agency work, the tool is wrong for you.

Fixed-fee project with milestone billing

Take a website redesign sold as a fixed-fee project. The statement of work includes discovery, design approval, and launch.

The clean workflow looks like this:

- Sales enters the signed contract and milestone values.

- Finance reviews the revenue policy tied to those milestones.

- Delivery marks each milestone complete when the client acceptance condition is met.

- The software recognizes the assigned portion of revenue and updates deferred balances.

This works well when milestone definitions are tight. It breaks when the contract says “design complete” but the team keeps revising for two more weeks. That is not a software flaw. It is a contract and process flaw.

Time and materials contract

Now take a consulting engagement billed on hours worked.

Here, the software should pull approved time by person, role, project, or task category. That data becomes the basis for earned revenue in the period, subject to the contract terms. Finance no longer waits for someone to summarize effort in a spreadsheet at the end of the month.

Agencies usually feel the operational gain first here. Revenue follows approved work instead of a delayed admin process.

Hybrid retainer with overages

A more realistic agency example is a monthly retainer that includes a base service level plus extra work above an agreed threshold.

That means you have at least two recognition streams:

- the retainer portion, usually recognized over the service period

- overage or extra project work, recognized based on the delivery rule tied to that work

If those overages involve implementation or customization, the accounting judgment gets harder. Cohen & Co. notes that deciding whether implementation services should be recognized at a point in time or over the contract term remains a major challenge, and ongoing customization makes that timing harder because one misclassification can ripple through the forecast (Cohen & Co. on software and SaaS revenue recognition challenges).

Where agencies usually get tripped up

The failure mode is rarely in the math. It is in the handoff.

A few warning signs:

- Milestones are subjective: Teams cannot agree what “complete” means.

- Change requests sit outside the contract record: Delivery knows the scope changed, finance does not.

- Support work bleeds into project work: The system cannot tell which rule applies.

- Time categories are too vague: Hours get logged, but not in a way that supports policy.

If your software needs constant manual overrides, it is usually exposing a policy problem or a data model problem. Treat the override count as a diagnostic tool.

The best workflow is boring. Contract terms come in clean. Work evidence lands in the system automatically. Exceptions are rare and reviewed, not routine.

Calculating the ROI of revenue recognition software

Agency owners often ask the wrong question first. They ask what rev rec software costs. The better question is what the current process is already costing in labor, delay, and bad decisions.

Manual close work is expensive even before you price it

When finance, ops, and delivery spend days reconciling contracts, hours, and billing, those hours are not just administrative. They displace planning work.

You lose time in places such as:

- finance rebuilding schedules

- PMs chasing completion status

- account leads clarifying scope changes

- leadership waiting on numbers they do not fully trust

That drag rarely shows up as one line item, which is why it gets tolerated for too long.

Better accuracy changes operating decisions

The financial value is not only in cleaner books. It is also in cleaner decisions.

When recognized revenue is tied to actual delivery data, leaders can make better calls about:

- whether a client is profitable

- whether a team is over-servicing retainers

- whether pipeline needs to convert faster to cover future capacity

- whether hiring should happen now or next quarter

Utilization data starts to matter here. If you want a better grip on the operational side of margin, this primer on how to calculate utilization rate is a useful companion because utilization and recognized revenue often drift apart when time capture is weak.

Risk reduction has real value

One bad spreadsheet formula can carry forward for months. A contract modification entered late can move revenue into the wrong period. An audit review can then turn into a scramble because nobody can show the chain of evidence.

Software does not remove judgment. It does reduce random inconsistency. That matters a lot in mid-sized firms where process maturity is still catching up with contract complexity.

The clearest ROI test

Ask four simple questions.

| Question | Why it matters |

|---|---|

| How long does month-end close take because of revenue cleanup? | This reveals labor waste |

| How often do people adjust schedules manually? | This reveals process fragility |

| Can ops and finance explain the same revenue number the same way? | This reveals system trust |

| Can you prove why revenue was recognized in a given period? | This reveals audit readiness |

If those answers are messy, the business case is usually already there.

A buyer's checklist for mid-sized agencies

Most vendor demos look good for the first fifteen minutes. Then you ask about a changed scope, a blended contract, or milestone proof, and the room gets quiet.

Use the checklist below as a working document during evaluation.

Agency rev rec software evaluation checklist

| Evaluation Criteria | Why It Matters for Agencies | Vendor Response (Yes/No/Details) |

|---|---|---|

| Handles fixed-fee milestones | Many agencies recognize revenue based on acceptance events, not simple monthly schedules | |

| Handles time and materials contracts | Hours often drive earned revenue directly | |

| Handles hybrid retainers and overages | Real agency contracts mix base service and variable work | |

| Stores contract amendments cleanly | Scope changes are common and must flow into recognition logic | |

| Integrates with CRM | Commercial terms should not be rekeyed by finance | |

| Integrates with ERP or accounting platform | Recognition needs a clean path into the ledger | |

| Accepts time and activity data | Agencies need delivery evidence, not just invoice data | |

| Supports clear audit trails | You need to prove who changed what and when | |

| Allows policy rules by service type | Strategy work, implementation, and support may follow different logic | |

| Supports deferred revenue reporting and forecasting | Leadership needs visibility, not just compliance output |

Questions worth asking in the demo

Do not ask whether the tool is “flexible.” Every vendor says yes. Ask harder questions.

- Show our contract types: Ask the vendor to model one milestone project, one T&M engagement, one hybrid retainer.

- Show a scope change mid-period: This tells you whether amendments are first-class records or awkward workarounds.

- Show the audit path: You want to see the exact source of recognized revenue, not a generic summary.

- Show exception handling: Every agency has edge cases. The issue is whether the system contains them cleanly.

What good answers sound like

Good vendors answer with process detail. They explain where the contract record lives, how changes propagate, and how users review exceptions.

Weak vendors answer with broad language about automation and visibility, then rely on CSV uploads and manual mapping for the hard parts.

Buy for the contract mess you already have, not the neat contract model you wish sales used.

A mid-sized agency does not need the most complex enterprise platform on the market. It needs one that fits service work, connects to operational data, and does not collapse under change.

Your next steps toward automated revenue recognition

Most agencies do not need a giant transformation project to improve revenue recognition. They need a cleaner operating model and a tighter system chain.

Step one, map the current mess

Write down how a contract becomes recognized revenue today.

Track the path from signed deal to delivery evidence to invoice to ledger. Mark every handoff, every spreadsheet, and every place where someone makes a judgment outside the system. That exercise alone usually explains why month-end feels harder than it should.

Step two, set policy before you shop

Do not ask software to solve disagreements your team has not resolved.

Clarify how you want to treat:

- milestone completion

- implementation work

- support and customization

- retainer overages

- scope changes and credits

When policy is vague, software just makes the confusion faster.

Step three, choose tools that connect operations to finance

The strongest rev rec setups in agencies connect commercial terms, delivery evidence, and accounting output. They do not treat finance as an island.

If you are also reviewing the accounting side of your stack more broadly, this roundup of cloud accounting software can help frame where the general ledger and reporting layer should fit.

The timing for getting this right is not arbitrary. The global revenue recognition software market was valued at approximately $2.5 billion in 2024 and is projected to grow at a 12% CAGR to reach $4.5 billion by 2029, driven by more complex service revenue and regulatory pressure. The same market analysis notes that automated tools help cut month-end close times from weeks to days (Market Report Analytics on revenue recognition software).

That growth matters because it reflects a broader shift. Revenue recognition is no longer a back-office cleanup exercise. For agencies, it is part of operational control.

When the contract record is clean, the delivery data is trustworthy, and the recognition rules are consistent, finance stops reconstructing the month after the fact. Leadership gets a revenue number they can run the business on.

If your agency wants cleaner activity data before it reaches billing and rev rec workflows, TimeTackle is worth a look. It helps teams capture work from calendars and connected systems with less manual effort, which makes utilization reporting, billing support, and downstream financial reporting easier to trust.